SOC 1 Report: A Complete Guide for Auditors 2026

Modern financial reporting relies heavily on third-party service providers. From payroll processors to cloud-based billing platforms, user entities frequently outsource processes that directly impact their financial statements. For auditors, this presents a significant challenge. Organizations cannot rely solely on vendor representations regarding control effectiveness. Organizations require verified, structured assurance.

The American Institute of Certified Public Accountants (AICPA) developed the Statement on Standards for Attestation Engagements 18 (SSAE 18) to address this exact issue. By establishing the framework for SOC 1 examinations, SSAE 18 introduced a standardized framework for evaluating service organizations, reducing reliance on ad-hoc vendor testing.

For audit and advisory teams, a SOC 1 is a critical audit dependency rather than just another piece of compliance documentation. This article explains how to navigate, evaluate, and execute these engagements effectively.

What is a SOC 1 Report?

A System and Organization Controls (SOC) 1 report is an independent attestation report that evaluates a service organization’s controls relevant to a user entity’s internal control over financial reporting (ICFR).

Issued under the SSAE 18 standard by the AICPA, a SOC 1 report is an attestation, not a certification. An independent CPA firm examines management’s assertion and issues an opinion on whether controls are suitably designed (Type I) and, in a Type II report, whether those controls operated effectively over a defined period.

If you are an auditor evaluating a service provider, you look to the SOC 1 to determine if the provider's processes can materially impact your client's financial statements. When service organization processes impact financial reporting, auditors may rely on SOC 1 reports to inform their audit approach.

Who Needs a SOC 1 Report?

A SOC 1 report applies to any service organization whose systems, services, or processes affect the financial reporting of its customers. If a provider makes an error that flows through to a client's balance sheet or income statement, a SOC 1 report is commonly requested in such scenarios.

Common examples of organizations that need a SOC 1 include:

Payroll processors: They handle wage calculations and tax withholdings.

Fintech platforms: They process financial transactions and manage ledgers.

Claims processors: They adjudicate medical or insurance claims that affect financial liabilities.

The "Do I Need a SOC 1?" Decision Checklist

If you are advising a service organization, use this simple checklist to determine if a SOC 1 is the right path:

Does the service process, store, or transmit financial data for clients?

Can a failure in the service directly cause a material misstatement in a client's financial records?

Are your services part of a control relied upon in your clients’ financial statement audits?

Are clients’ external financial auditors requesting assurance over the service?

Does the service involve executing financial transactions on behalf of users?

If the answer to any of these is yes, a SOC 1 examination is usually the appropriate next step.

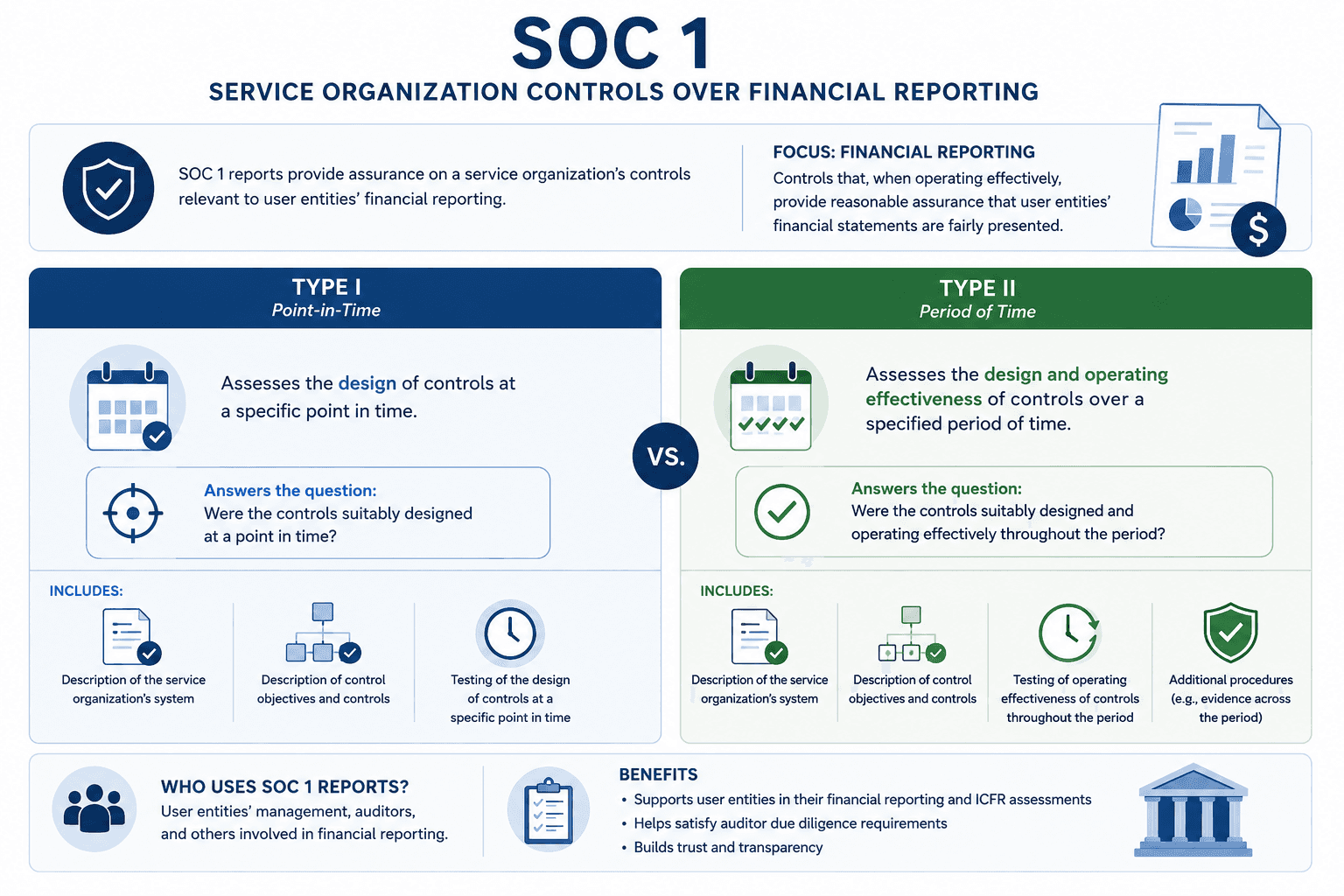

SOC 1 Type I vs Type II: What Auditors Actually Look For

When evaluating or issuing a SOC 1, you must understand the distinction between the two types of reports.

Type I: This report evaluates the design of controls at a specific point in time. It answers the question: Has management designed controls that are suitable to achieve the stated control objectives?

Type II: This report evaluates both the design and operating effectiveness of controls over a specified period (typically 6 to 12 months). It answers the question: Did these controls actually function as intended over the review period?

Auditors of user entities generally prefer Type II reports, as they provide evidence of operating effectiveness over time. While a Type I can help a service organization establish a baseline during its first year, it provides limited value to an external financial auditor because it does not prove that the controls worked consistently.

Feature | SOC 1 Type I | SOC 1 Type II |

Focus | Design of controls | Design and operating effectiveness |

Timeframe | Point in time | Period of time |

Testing Depth | No testing of operating effectiveness | Tests of controls using sampling, inspection, inquiry, and re-performance |

Auditor Reliance | Limited | Greater (subject to evaluation) |

Inside a SOC 1 Report: Structure and Key Sections

A standard SOC 1 report follows a specific structure. Knowing how to navigate these sections is essential for user auditors who need to extract relevant information quickly.

Independent Service Auditor’s Report: This is the report’s official opinion. The CPA firm states the audit is unqualified or qualified. A qualified report includes exceptions.

Management Assertion: Service organization leadership writes this statement. They confirm the system description and control design. Management asserts that controls are suitably designed and, for Type II reports, operated effectively over the specified period.

System Description: The system’s boundaries include design, infrastructure, systems, processes, and personnel.

Control Objectives & Controls: This section outlines the organization’s control objectives and corresponding controls.

Tests of Controls (Type II only): This section provides the testing procedures performed by the auditor and the results of those tests.

Complementary User Entity Controls (CUECs): These controls are the user entity’s controls that the service organization depends on.

Subservice Organizations: The report may describe third-party providers using either the carve-out or inclusive method.

Understanding Control Objectives vs Controls (With Examples)

For a SOC 1 evaluation to be successful, one must understand the association of objectives, controls, and risks in a given framework.

Control Objectives: Control objectives define the intended outcomes of controls in addressing risks related to financial reporting.

Controls: These are the specific policies, procedures, or system designs put in place to attain control objectives and are meant to function uniformly and continuously.

Here is a common mapping format used in the industry:

Objective: Controls provide reasonable assurance that for a given program or data, only authorized users retain access.

Control: In the financial processing application, for access to be granted to a user, multi-factor authentication (MFA) must have been completed, and user access rights are subject to review of a designated individual on a regular basis (quarterly).

Risk Addressed: Permitting an unauthorized user to access the system may lead to unintended modifications of the financial data and, hence, an erroneous financial report.

Without sufficiently organized tools or set workflows, managing these mappings across various clients and systems can become overly complex.

The SOC 1 Audit Process: Step-by-Step Breakdown

If you are guiding a service organization through a SOC 1, the process generally follows a structured sequence of steps:

Scoping: Identify the systems, locations, and processes that are relevant to user entities' financial reporting.

Readiness Assessment: Before the actual audit, perform a gap analysis to find out what controls are missing or poorly designed.

Control Design & Documentation: The service organization implements required controls, updates policies, and starts to produce evidence.

Auditor Fieldwork: The independent CPA firm reviews evidence and performs walkthroughs, assesses control design, and conducts testing (for Type II engagements).

Testing of Controls (Type II): During the review period, the auditor selects samples and performs inspection, inquiry, and reperformance to evaluate operating effectiveness.

Final Report Issuance: After testing finishes, the CPA firm reviews results, forms a conclusion, and produces the SOC 1 report.

SOC 1 Readiness vs SOC 1 Audit: What’s the Difference?

Service organizations often confuse the audit with the readiness assessments.

Readiness Assessment: Can be done internally and is typically performed by internal teams or advisors. Primarily focuses on gap identification and control design improvement. No independent opinion emerges from this.

SOC 1 Audit: Must be undertaken by an outside CPA firm in line with SSAE 18. This leads to an official attestation.

Skipping the readiness assessment may result in control deficiencies or other exceptions being found during the audit. If a service organization directly conducts a Type II audit, and controls have not been designed and exercised appropriately, the auditor may identify control exceptions during testing.

How Auditors Evaluate SOC 1 Reports

When reviewing a SOC 1 report from a service provider, the objective is to determine whether, and to what extent, the report can be used to support the audit approach.

Key areas of evaluation include:

Control Relevance: Do the control objectives actually cover the financial assertions relevant to your client?

Testing Results: Are exceptions noted in the testing section? If so, has management provided an adequate response, and do the exceptions indicate isolated issues or broader control deficiencies?

Coverage Period: Does the Type II period align with your financial audit period? If not, you may need a bridge letter (gap letter).

Subservice Organizations: Did the service provider carve out a critical vendor (like a cloud hosting provider)? If so, you must evaluate that vendor's SOC report as well.

Red Flags to Look For: Watch out for vague system descriptions, repetitive control exceptions in access management, and missing CUEC documentation.

Common Mistakes Organizations Make with SOC 1

Service organizations often face challenges when navigating the SOC 1 lifecycle. Potential pitfalls can be identified to help better assist your clients.

Misaligned Scope: Services include systems that are not relevant to financial reporting, leading to a loss of time and money.

Weak Control Documentation: Failing to capture the "who, what, when, and how" of a control activity.

Ignoring CUECs: Failing to address Complementary User Entity Controls (CUECs) may lead to control gaps at the user entity level.

Poor Evidence Retention: Control is operated correctly, but the necessary backup, such as screenshots, sign-offs, or logs to demonstrate it to an auditor, is insufficient.

Overly Generic Control Descriptions: Controls described at a high level without sufficient specificity to evaluate design or testing.

How Roz Supports SOC 1 Engagements

For CPA firms and advisory teams, managing SOC 1 documentation, extracting controls, and drafting workpapers is historically a manual, error-prone process. Roz is an AI-native engagement and audit-delivery platform designed to structure and accelerate this work.

Roz can support your audit workflows by acting as an intelligent enterprise data room.

Structured Documentation Workspaces: Centralize client policies, procedures, and evidence in secure, client-specific workspaces.

Control Extraction and Mapping: Extract controls from uploaded policies and support structured mapping for comparison against framework requirements.

AI-Assisted Draft Workpapers: Generate draft workpapers and report sections from firm templates, with audit trails linking back to source evidence.

First-Pass Control Testing Support: Support documentation review by highlighting potential evidence gaps and sufficiency issues early.

By structuring documentation and supporting first-pass analysis, Roz helps firms improve traceability and manage engagement workflows more efficiently, without replacing auditors or certification bodies.

Conclusion

An SOC 1 report is not only a compliance requirement but also an important component of trust in financial reporting processes. It adds value when organizations understand control design, operating effectiveness, and auditor expectations.

When assessing a client’s vendor report, or when a client is preparing for their first audit, always push for a comprehensive readiness phase. This will help to minimize findings, optimize the audit, and deliver the assurance that the financial ecosystem requires.