SOC 3 Compliance: Everything You Need to Know

As businesses handle more sensitive information, potential customers often ask for security validation earlier in the sales process. Showing that you have a mature security posture can help build trust and support enterprise purchasing decisions.

A System and Organization Controls 2 (SOC 2) report provides a detailed look at an organization's security and operational controls. However, it often contains sensitive operational information and is typically shared under non-disclosure agreements. Because of this limited distribution, it can be difficult to communicate assurance broadly. A SOC 3 report addresses this challenge by providing a public-facing summary of an organization's control environment.

This article is for SaaS companies, startup founders, compliance teams, and CPA firms looking to better understand SOC 3. You will learn what SOC 3 is, when it makes sense to pursue it, the steps involved in obtaining a report, typical costs and timelines, and how AI-native platforms like Roz can support engagement workflows.

What is SOC 3 Compliance?

A SOC 3 report provides a high-level overview of an organization’s internal controls. This report is a public-facing independent assurance report. SOC 3 reports are based on the Trust Services Criteria defined by the American Institute of Certified Public Accountants (AICPA), similar to SOC 2 reports.

Because the report requires an independent CPA, customers, partners, and stakeholders perceive it as credible. A notable feature of a SOC 3 report is its public audience. These reports are most commonly accompanied by a SOC 2 report, and unlike a SOC 2 report, a SOC 3 report excludes sensitive system details and detailed control testing results.

This allows organizations to share SOC 3 reports publicly. Organizations can disseminate it publicly to comply with requirements for integrity of security and reliability of operations. Organizations can also post SOC 3 reports to areas of their website that demonstrate their commitment to operational effectiveness and reliability.

What is Included in a SOC 3 Report?

A typical SOC 3 report is concise and contains the following components at a minimum:

Independent auditor opinion: This is the CPA’s assessment of whether the organization’s internal controls are effectively designed and operating effectively to meet one or more Trust Services Criteria

Management assertion: This is a statement of the management of a company and an organization’s control system.

System Description: This is an overview of the organization’s control system and the services and infrastructure environments that support the system.

Trust Services Criteria: This criterion defines which of the Trust Services Criteria are within the audit, for example, security, availability, integrity, confidentiality, and privacy.

High-level control effectiveness: Overall summary of the design and operational effectiveness of controls during the review period.

What SOC 3 Does Not Include

The SOC 3 report purposefully omits certain aspects of a SOC 2 report to ensure sensitive operational concerns are protected. These aspects typically involve specific control testing and samples of evidence, as well as broad descriptions of risks.

Further, SOC 3 reports typically refrain from including sequential control descriptions, intricate architecture designs, or specific technical settings. These restrictions allow organizations to provide assurance publicly while minimizing the risks of disclosing sensitive operational or security information.

SOC 1 vs SOC 2 vs SOC 3: What’s the Difference?

Organizations can determine which SOC report best fits their business and customer requirements by understanding the differences between the three main types.

Feature | SOC 1 | SOC 2 | SOC 3 |

Purpose | Evaluates controls impacting financial reporting (ICFR) | Evaluates security and operational controls | Public summary of SOC 2 examination |

Framework | SSAE 18 / AT-C 320 | Trust Services Criteria (AICPA) | Trust Services Criteria (AICPA) |

Focus Area | Financial reporting controls | Security, availability, confidentiality, privacy, processing integrity | Same as SOC 2 (high-level summary) |

Audience | Client auditors, CFOs, finance teams | Customers, partners, compliance teams | General public and prospects |

Detail Level | Detailed financial control testing | Detailed operational and technical testing | High-level summary only |

Distribution | Restricted use | Restricted use (often NDA) | Publicly shareable |

Type I Available | Yes | Yes | No (derived from SOC 2) |

Type II Available | Yes | Yes | Typically based on SOC 2 Type II |

Includes Testing Evidence | Yes | Yes | No |

Includes Exceptions | Yes | Yes | No |

Use Cases | Payroll, financial SaaS, payment processors | SaaS, cloud providers, technology vendors | Trust centers, marketing, early sales |

Certification Type | Attestation | Attestation | Attestation |

Public Trust Purpose | Limited | Limited | Primary purpose |

Typical Duration | 1-3 months | 3-6 months (Type II) | Issued after SOC 2 |

SOC 1 focuses on controls related to financial reporting, while SOC 2 and SOC 3 evaluate security and operational controls based on the Trust Services Criteria. SOC 2 provides detailed information to support customer due diligence, whereas SOC 3 offers a high-level summary designed for broader sharing. Organizations often use SOC 2 for vendor risk assessments and SOC 3 to support trust centers and communicate transparency during early sales conversations.

Who Should Consider a SOC 3 Report?

While no regulations mandate a SOC 3 report, organizations often pursue it to publicly demonstrate their security posture and control environment. SOC 3 reports are particularly useful for organizations that handle customer data and want to build trust with prospective customers during early sales conversations.

Typical SOC 3 applicants include:

SaaS companies

Cloud hosting providers

Fintech platforms

Infrastructure providers

Healthcare technology companies

Third-party data processors

SOC 3 reports are beneficial for prospective customer trust and preliminary sales conversations. Customers are able to assess SOC 3 reports and obtain a summary of assurance without signing a non-disclosure agreement or undertaking a vendor risk assessment.

SOC 3 Trust Services Criteria Explained

SOC 3 examinations are based on the Trust Services Criteria (TSC) established by the American Institute of Certified Public Accountants (AICPA). Depending on the customer commitments, organizations can choose one or multiple criteria.

Security (Required): Evaluates how an organization protects systems and data, including access controls, monitoring, and risk management.

Availability: This is to assess the company on its uptime. This includes their method of backup, data recovery, and how they keep the business operational.

Processing Integrity: This refers to how a company processes information. Whether it is timely, accurate, and complete.

Confidentiality: This refers to how companies deal with sensitive information and which line of control they put in place to avoid information tampering.

Privacy: This is where companies assess how they collect and dispose of data.

Security is required for SOC 3 examinations, while the other criteria are optional based on scope and customer commitments.

SOC 3: Type I vs Type II

A common misconception is that SOC 3 reports are issued as Type I or Type II. However, SOC 3 reports do not have Type I or Type II designations.

SOC 3 reports are typically issued alongside SOC 2 reports. A SOC 2 Type I report evaluates the design of controls at a specific point in time, while a SOC 2 Type II report assesses the operating effectiveness of controls over a defined observation period, usually between 3 and 12 months.

Because SOC 2 Type II reports evaluate control performance over time, SOC 3 reports are most commonly based on SOC 2 Type II examinations, as they provide a higher level of assurance for public distribution.

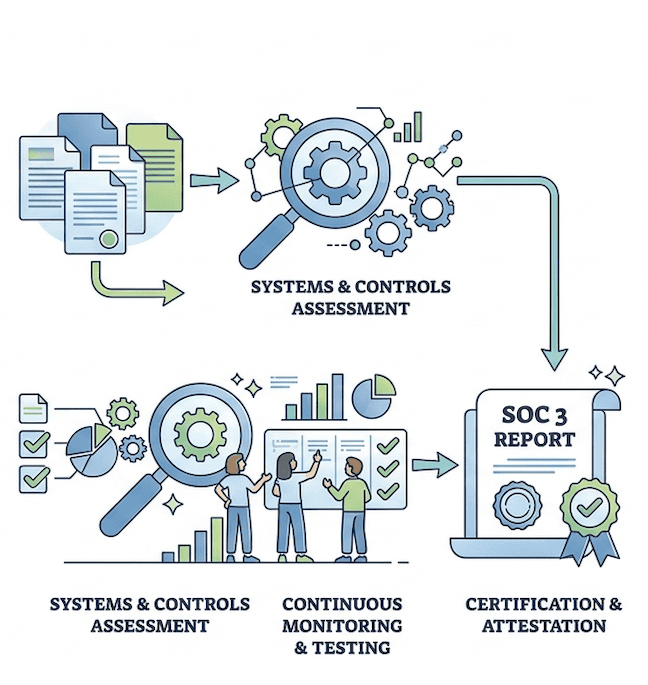

How to Get SOC 3 Compliance

Receiving a SOC 3 report is generally a step-by-step process:

Step 1: Define Scope

Establish which systems, services, and locations will be reviewed. From there, determine applicable trust services criteria based on your business model.

Step 2: Implement Controls

Develop operational processes and security policies, such as access control, monitoring, and incident response.

Step 3: Perform Readiness Assessment

Prior to the audit, conduct a gap analysis to find any missing controls or documentation.

Step 4: Undergo SOC 2 Audit

Hire an independent CPA firm to assess controls, review documentation, and issue the SOC 2 report.

Step 5: Issue SOC 3 Report

After completing the SOC 2 report, the same CPA firm will draft a SOC 3 report. This report provides a high-level overview, omitting critical details, and is suitable for external sharing.

How Much Does SOC 3 Cost?

The price of a SOC 3 report varies and is influenced by the Trust Services Criteria, system complexity, company size, and the existing control frameworks.

Cost components typically include the following:

Readiness assessment or a gap analysis

External audit fees

Internal resource allocation

Compliance tooling or automation platforms

Because SOC 3 is typically issued alongside a SOC 2 examination, organizations typically incur minimal additional cost for the SOC 3 report itself. The bulk of the expense is attributed to the SOC 2 audit. Depending on the scope and the auditor, SOC 2 engagements typically range between $10,000 and over $60,000. The SOC 3 report is often included in the audit fee or provided at a minimal additional cost as part of the overall engagement.

Actual costs vary based on the complexity of the organization and the scope of the audit.

How Long Does SOC 3 Take?

The timeline for obtaining a SOC 3 report depends primarily on an organization’s readiness. Preparing documentation, implementing controls, and conducting a readiness assessment can take several weeks to a few months, depending on the maturity of the control environment.

Because SOC 3 reports are typically issued alongside SOC 2 examinations, the timeline largely follows the SOC 2 audit process. A SOC 2 Type I audit usually takes about 4 to 8 weeks, while a SOC 2 Type II audit requires an observation period, typically ranging from 3 to 12 months, to evaluate control effectiveness over time.

Once the SOC 2 audit is completed, the SOC 3 report is generally issued shortly afterward as part of the same engagement.

How Roz Accelerates SOC 3 Engagement Delivery

SOC 3 engagements often involve heavy documentation, evidence organization, and manual workpaper preparation. CPA firms and advisory teams must scale delivery while maintaining audit quality.

Roz is an AI-native engagement platform that helps streamline these workflows. Acting as an intelligent enterprise data room, Roz provides client-specific workspaces that help teams maintain structure across engagements.

Roz supports teams by:

AI-assisted draft workpapers with audit trails.

Evidence organization and traceability linked to source documentation.

Questionnaire assistance using uploaded client policies.

Control extraction and gap analysis to support documentation review.

By structuring documentation and supporting first-pass analysis, platforms like Roz help teams improve workflow efficiency and reduce manual coordination during SOC 3 engagements.

Conclusion

A SOC 3 report can be a useful way to show that an organization takes data protection seriously and values transparency. It provides a high-level, public-facing overview of an organization's security and control environment, based on the same examination as a SOC 2 audit.

By implementing mature internal controls and using structured engagement workflows, organizations can make the audit process more efficient. A SOC 3 report can also help build trust, support early sales conversations, and strengthen credibility with prospective customers.

FAQs

Is SOC 3 better than SOC 2?

Neither report is inherently better; they serve different purposes. SOC 2 provides detailed technical assurance intended for restricted audiences under an NDA. SOC 3 provides a high-level summary suitable for marketing and public trust centers.

Does SOC 3 expire?

SOC reports represent an evaluation over a specific timeframe. They do not technically "expire," but they typically become stale after one year. Organizations generally undergo annual audits to maintain a current and relevant compliance posture.

What is SOC Level 3?

"SOC Level 3" is a common misnomer. The correct terminology is a SOC 3 report. It refers to the third reporting option in the AICPA’s System and Organization Controls framework, rather than a tiered level of security clearance.