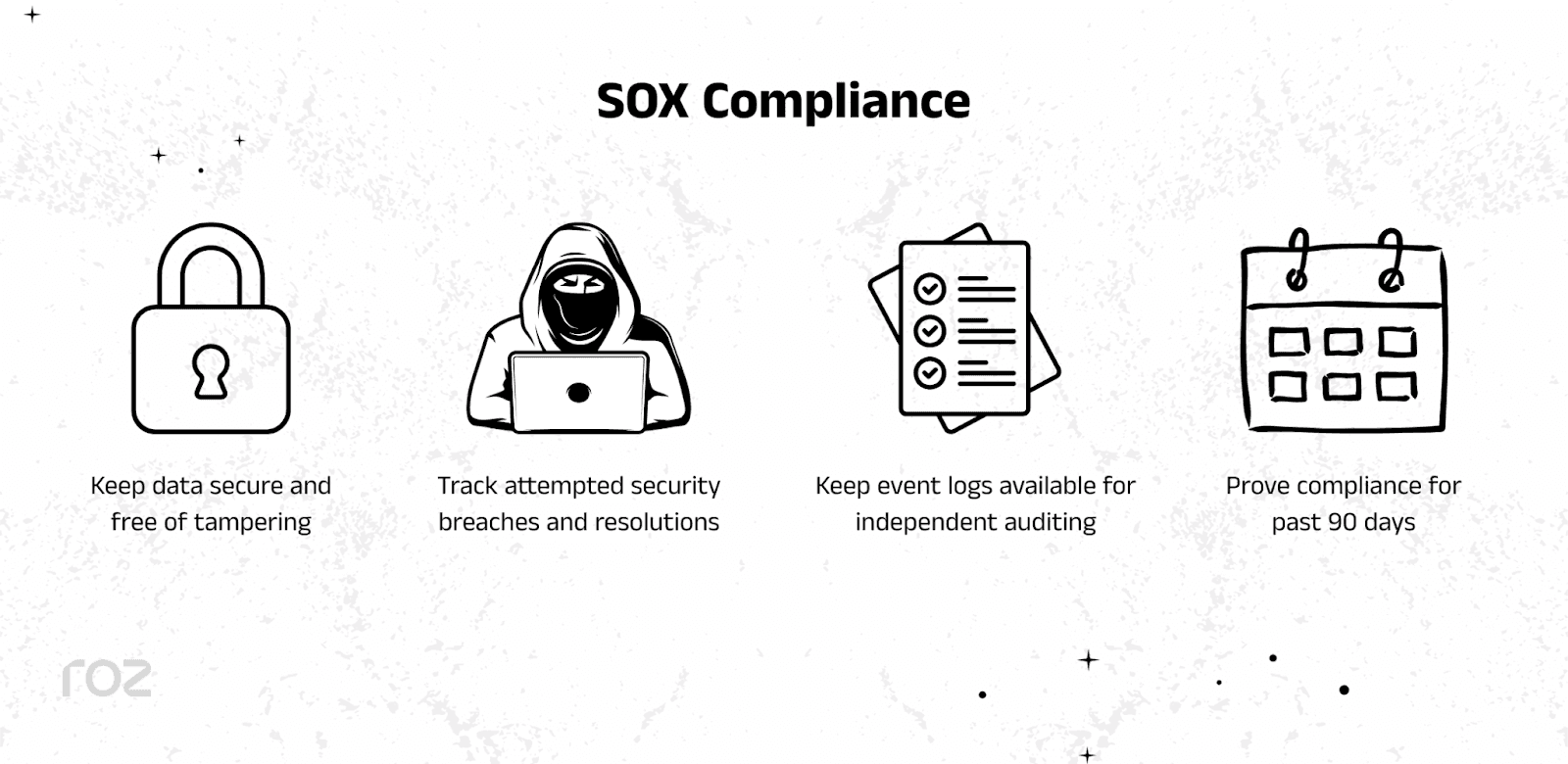

SOX Compliance: Requirements, Controls, and Audit Guide

SOX Compliance: Requirements, Controls, and Audit Guide

The early 2000s had corporate financial scandals involving Enron, WorldCom, and Tyco that cost investors billions and undermined confidence in U.S. capital markets. In response, Congress enacted the SOX to strengthen corporate accountability and transparency by requiring companies to establish and maintain effective internal controls over financial reporting.

For over 20 years, SOX has shaped financial reporting and governance practices for public companies in the United States. SOX is one of the most influential financial compliance laws affecting public companies and their reporting obligations. Public companies must comply with its requirements, which include establishing and maintaining internal controls over financial reporting and undergoing periodic audits.

In this article, I will explain SOX compliance, including who it applies to, the most relevant sections, the process for designing and assessing controls, and the impact of the audit technology provider. Roz is transforming SOX readiness for CPA firms and their clients.

What Is SOX Compliance?

SOX compliance ensures that the company is in accordance with the Sarbanes-Oxley Act of 2002, a federal law enacted to protect investors and safeguard the accuracy and reliability of corporate financial disclosures.

The act established strict standards for:

Executive accountability: CEOs and CFOs must sign off on the accuracy of financial statements.

Internal controls: Companies must develop, implement, and evaluate their own controls over financial reporting.

Independent audits: External auditors must confirm the management's evaluation of the internal control systems.

Transparency: Companies are required to disclose any material changes to their financial condition immediately.

Overseen By

Two federal bodies supervise compliance with SOX:

Securities and Exchange Commission: Enforces SOX rules and investigates violations.

Public Company Accounting Oversight Board: Oversees and audits the accounting firms that conduct audits of public companies.

Who Must Comply with SOX?

SOX compliance is mandatory for:

Public companies: Companies whose securities are registered under section 12 of the Securities Exchange Act or are required to report under section 15(d) are public companies.

Foreign issuers listed in the U.S.: If a foreign company lists its securities on a U.S. stock exchange (like the NYSE or NASDAQ), it becomes subject to SOX.

IPO-stage companies: Private companies that are preparing to go public will usually start to implement SOX controls in the pre-IPO period.

Subsidiaries impacting consolidated financials: If a subsidiary's financial data is significant enough to affect the financial reporting of the parent company, SOX controls are applicable.

Do Private Companies Need SOX Compliance?

There is no legal obligation for private companies to comply with SOX. Still, many private companies choose to implement SOX-like controls because:

Investors and lenders expect strong financial governance.

The SOX framework encourages operational discipline and reduces the likelihood of fraud.

The company is aligned and ready for an IPO or a public company acquisition.

Why Is SOX Compliance Important?

Investor Protection

SOX compliance ensures that investors are protected, as they are guaranteed access to correct and relevant financial details. For investors to be able to put their faith in the market, SOX allows a guarantee that the reporting is legally enforceable.

Executive Accountability

CEOs and CFOs are individually responsible under Section 302, and each is required to certify:

The financial report has been reviewed.

There are no material misstatements or omissions in the report.

The financial statements adequately present the company's condition.

The disclosure controls are effective.

False certification can result in criminal penalties, including fines up to $5 million and imprisonment for up to 20 years.

Fraud Prevention

Section 404 requires management to assess and report annually on the effectiveness of internal control over financial reporting. For most public companies, external auditors must also attest to this assessment. This forces organizations to identify and remediate control weaknesses before they lead to material misstatements.

Stronger Governance & Audit Readiness

SOX makes companies better with:

Documentation quality: Policies, procedures, and evidence must be thorough and accessible

Control design: Financial processes are reviewed and streamlined.

Audit efficiency: Well-documented controls make external audits faster and less expensive

Reduced Financial Misstatement Risk

SOX requires companies to document and test internal controls over financial reporting. Strong internal control programs required by SOX can reduce the likelihood of financial misstatements and improve the reliability of financial reporting.

SOX Compliance Requirements Explained

At a high level, SOX compliance has 4 primary requirements:

Submit audited financial statements to the SEC.

Report material changes to your financial condition or operations.

Design, implement, and test your internal controls over financial reporting.

Provide a management report annually on the effectiveness of ICFR.

Section 302 - Executive Certification

Section 302 requires that the CEO and the CFO must certify in each quarterly and annual report the following:

They are responsible for the creation and execution of the necessary disclosure controls and procedures.

They have assessed the effectiveness of the controls in the 90 days that are before the report.

They have reported all the material weaknesses to the auditors.

They have reported any fraud that involves significant personnel in the internal controls.

Disclosure controls and procedures are regarded as the controls that guarantee information required to be presented in SEC filings is noted, processed, summarized, and reported in the required time frame.

Section 404 - Internal Control Reporting

Section 404 is the most operationally demanding. It includes the following:

Managerial evaluation: An annual report of the effectiveness of ICFR is required.

Auditor involvement: The auditors require an independent evaluation, review, and report of the manager's evaluation.

Document retention: Evidence showing support for the company's ICFR evaluation must be kept.

ICFR is a process that is designed to give reasonable assurance that:

All financial reporting is reliable.

The financial statements are prepared in accordance with GAAP.

Records are kept that accurately document and reflect the transactions and dispositions of the assets.

Transactions are recorded to support adequate financial statement preparation.

We timely detect and prevent unrestricted access to assets that could materially affect the financial statements.

Material weakness: An internal reporting control deficiency that, in isolation or in combination, likely allows a material misstatement of the annual or interim financial statements to occur.

Significant deficiency: A deficiency or a combination of deficiencies that is not a material weakness or strength but is important enough to justify the concern of the parties in control of the financial reporting.

If any material weaknesses exist, management cannot conclude that ICFR is effective.

Record Retention & Documentation

Section 802 requires the following:

Audit workpapers are to be kept for 7 years.

Fraudulent destruction, alteration, or concealment of records to obstruct federal investigations is a crime that can lead to fines, imprisonment, or both.

Financial Disclosure & Reporting

Companies are required to:

File timely periodic reports (10-Q, 10-K).

Submit off-balance sheet disclosures.

Avoid misleading reporting with pro forma figures.

Report all material changes in a timely manner (Section 409).

SOX Internal Controls: Types and Examples

SOX internal controls include procedures and policies that help guarantee that financial reporting is accurate and reliable. The majority of companies use the COSO framework to develop ICFR programs. Internal control reports generally consist of the following types of controls.

Entity-Level Controls (ELCs)

These controls are high-level and set the “tone at the top” and shape the environment of the controls.

Audit committee oversight: The audit committee is independent and has a member who is a financial expert.

Code of conduct: Ethics policies and whistleblower protections.

Tone at the top: Leadership that is fully committed to integrity and compliance.

Risk assessment processes: Systematic identification of financial reporting risks.

Process-Level Controls

These are particular controls within business processes:

Revenue recognition controls: Approval of sales contracts and validation of delivery.

Accounts payable approvals: Segregation of duties in requisitioning, approval, and payment.

Payroll validation: Review of payroll reports and authorization of changes.

Reconciliations: Reconciliations of accounts, bank reconciliations, and variance analysis.

IT General Controls (ITGCs)

ITGCs ensure that the IT systems that support the financial reporting are reliable and secure.

User access management: Role-based access, access reviews at set intervals, and timely removal from access control.

Change management: Approval, testing, and documentation of changes in the system.

Backup & recovery: Regular backups, tested restoration procedures.

Segregation of environments: Separation of development, testing, and production systems.

Application Controls

These are controls embedded in software applications:

Automated calculations: System-enforced formulas, for example, tax calculations.

Three-way match: Purchase order, receiving report, and invoice validation.

System validations: Data entry edits, required fields, limit checks.

Preventive vs. Detective Controls

Control Type | Purpose | Example |

Preventive | Stop errors before they occur | Segregation of duties, system access restrictions |

Detective | Identify errors after they occur | Account reconciliations, variance analysis, automated alerts |

Effective ICFR relies on a combination of both.

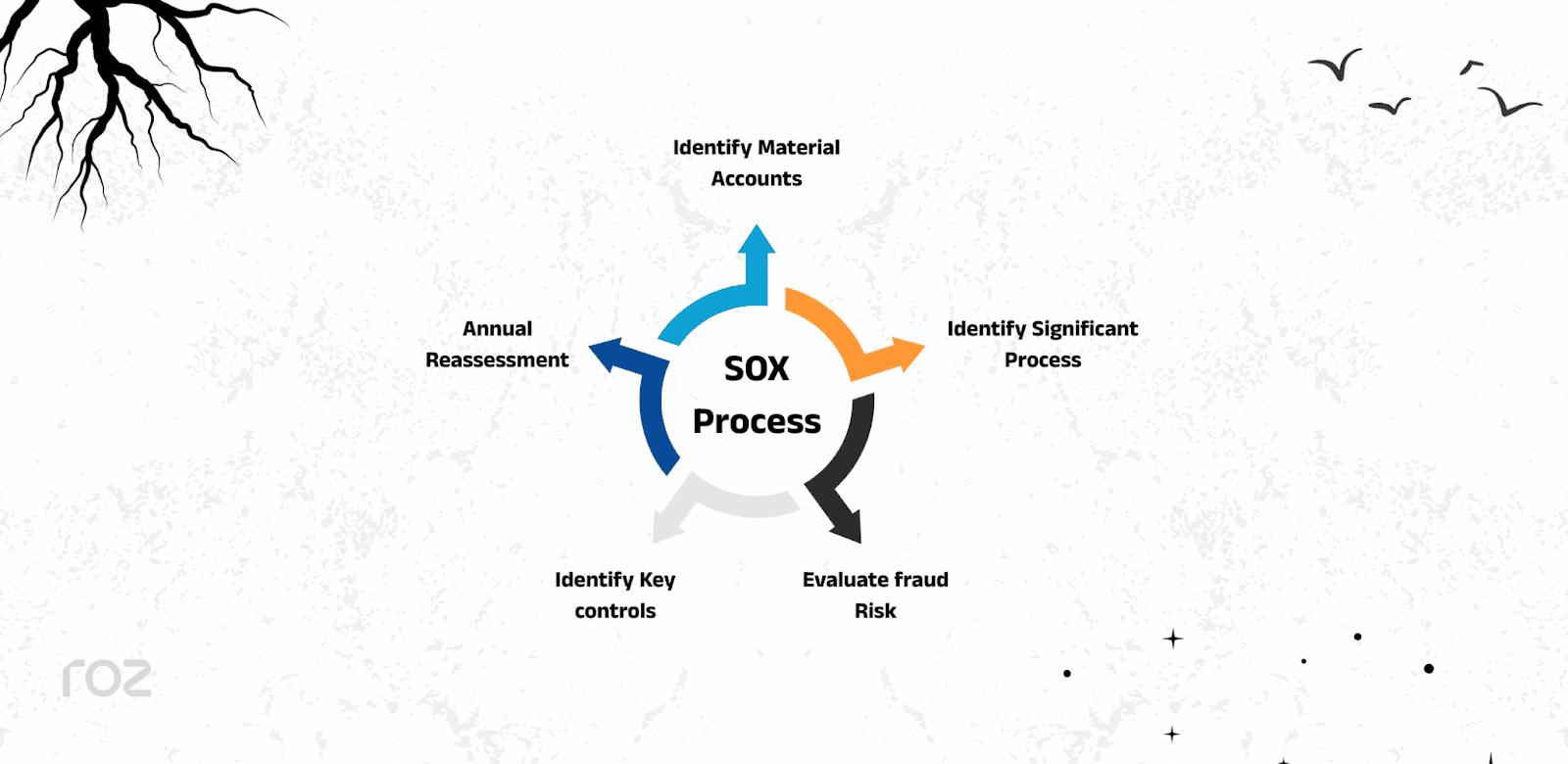

SOX Risk Assessment Process

Audits conducted by SOX examine the top-down risks to see where the greatest need for controls exists.

Step 1 - Identify Material Accounts

Identify which of the accounts and disclosures present in the financial statements are of importance because they can contain a misstatement that may be considered material, whether individually or when combined with other accounts.

In the materiality of a financial report, alignment usually falls within that range, and a combination of quantitative and qualitative is the basis. Quantitatively, the measure is expressed as a % of the total assets, while qualitatively, it is expressed as the number of accounts that are prone to fraudulent activity.

Step 2 - Identify Significant Processes

Trace the material accounts to the company processes that create or result in the material accounts. Such processes include the following:

The revenue cycle encompasses sales and accounts receivable.

The procurement cycle encompasses purchasing and accounts payable.

Payroll cycle.

Financial close and reporting.

Step 3 - Evaluate Fraud Risk

The areas where fraud could occur must be assessed in terms of the following:

Opportunity (e.g., weak segregation of duties)

Incentive (e.g., management bonuses tied to earnings)

Rationalization (e.g., pressure to meet targets)

Step 4 - Identify Key Controls

Identify the most important controls that are essential to avoiding material misstatements for each critical process. Controls are tested only for the most important ones associated with a higher level of risk.

Step 5 - Annual Reassessment

ICFR is dynamic. Companies need to assess risks every year, considering the following:

Changes in business processes.

New IT systems.

Acquisitions or divestitures.

Organizational restructuring.

The SOX Audit Process

SOX audits are consistent with the methodology prescribed by PCAOB Auditing Standard 2201 (AS 2201).

1. Planning & Scoping

Auditors:

Analyze the company and the industry.

Identify key accounts and disclosures.

Analyze the risk for material misstatement.

Decide which controls to test.

2. Walkthroughs

Auditors trace a transaction from the starting point to the recording in the financial statements to

Confirm the understanding of the process.

Identify areas where misstatements can occur.

Verify that controls are in place.

3. Design Effectiveness Testing

Auditors determine if controls may allow material misstatements to not be present or be detected. Methods may be:

Reviews of the policies and procedures.

Reviews of the configurations of the system.

Interviews with the owner of the controls.

4. Operating Effectiveness Testing

Auditors test if controls are functioning throughout the duration of the period under review. Methods can involve:

Inquiry: Asking control owners how the control is done (note that inquiry is considered the weakest evidence and needs to be supported by other methods).

Observation: Watching the control in action (a process).

Re-performance: Independently executing the control (e.g., recalculating a reconciliation)

Inspection: Examining evidence (e.g., approvals, logs, reports)

5. Deficiency Evaluation

Auditors classify each deficiency that is found:

Control deficiency: A deficiency in the design or operation of a control that does not permit management or employees to prevent or detect misstatements on time.

Significant deficiency: Less severe than a material weakness, but still important enough to warrant attention from those responsible for overseeing the company's financial reporting.

Material weakness: There is a reasonable possibility that a material misstatement of financial statements will go unapprehended or undetected.

6. Final Reporting

The final step is for the auditors to prepare and submit a final report and provide their opinion concerning the effectiveness of the company’s ICFR. Possible opinions include the following:

Unqualified: Indicative of ICFR being designed and operating effectively. This is the most favorable opinion a company can receive.

Adverse: Issued when one or more material weaknesses have been identified.

Disclaimer: This is issued when an auditor cannot complete all necessary work to reach an opinion, resulting in a limited audit scope.

Common SOX Audit Findings (And How to Avoid Them)

Weak IT Access Controls

Issue: Some of the users possess access beyond their role; users share their logins; access reviews are not done routinely; and delays exist regarding the removal of access to the system after termination.

How to Avoid:

Implement role-based access control (RBAC)

Review and recertify access and document the reviewer's evidence every quarter.

Access should be removed without delay upon termination.

Monitoring and access to privileged information should be controlled and reviewed separately.

Inadequate Segregation of Duties

Issue: The same person has the potential to initiate, approve, and record transactions, and this increases the potential of fraudulent activities.

How to Avoid:

Map roles to ensure separation of duties

Create system-enforced workflows that require approval.

Implement additional means of control (e.g., management review) if the segregation of control is not achievable.

Incomplete Documentation

Issue: Policies exist, but they are outdated, or there is no proof that controls have been exercised.

How to Avoid:

Keep previous documentation for version-controlled systems.

Control ownership and control frequency should be clearly defined and assigned.

Include timestamps with preparer/reviewer sign-offs.

Use a centralized repository for evidence retention.

Late or Missing Reconciliations

Issue: There now exists a lack of timeliness surrounding the completion of account reconciliations (not done, not reviewed, not supported).

How to Avoid:

Establish strict closed calendars.

Reconciliation workflows should be automated.

Create a requirement for both the preparer and the reviewer to close the sign-off.

Monitor the aging of reconciling items.

Poor Change Management Controls

Issue: System changes that are done without the following: testing, documentation, or approval.

How to Avoid:

Put in place a formal process for change requests and approvals.

Mandate testing in non-production systems.

Maintain documented change logs with evidence of approval.

Review emergency changes after implementation.

How Roz Supports SOX Engagement

SOX engagements are documentation-heavy and time-sensitive. We are an AI-native audit-delivery platform built to help CPA and advisory firms streamline control-based SOX engagements through structured workflows and first-pass automation.

Reduce Manual Work: Our tool generates first-pass workpapers using your firm's templates and client evidence, complete with audit trails. This cuts down drafting time, freeing auditors to focus on analysis.

Structure Evidence: Our tool extracts controls from documents, maintains a structured control library, and maps evidence to control objectives, improving organization and traceability.

Improve Consistency: By using firm-configured templates and workflows, Roz standardizes documentation, which enhances review efficiency and quality.

Support Readiness: Our tool performs gap analyses by reviewing documentation against control requirements, helping firms identify and address issues early.

Book a demo with us to see how our AI-native platform can transform your SOX engagements.

Conclusion

SOX compliance is NOT just a legal necessity; it is a competitive edge. Strong internal controls can not only reduce mistakes and accelerate the financial closing process but also increase the confidence of investors and improve the management of risk. For the executives, it strengthens responsibility, and for the market, it restores confidence. Although SOX compliance requires significant work, the right tools and mindset can transform it from a burden to a testament to your company's integrity, transparency, and strict compliance.

I hope this article has helped you learn everything you need to know about SOX compliance!

FAQs

Who is responsible for SOX compliance?

It is the CEO and CFO of the company. The finance, IT, internal audit, and compliance teams collaborate on the implementation.

How long does SOX compliance take?

SOX will require a company 6 to 12 months to initially comply, depending on the size and control maturity of the company. The cycles repeating this process are annual.