Continuous Auditing vs Continuous Monitoring Explained

If you work in audit, risk, or compliance, you have probably heard "continuous auditing" and "continuous monitoring" used as if they mean the same thing. They don’t. While they rely on similar technology, they answer different questions and produce different outcomes.

Many organizations are moving away from annual, point-in-time reviews because transaction volumes are growing and regulators expect ongoing evidence of control effectiveness. As more teams adopt automation, the line between auditing and monitoring can get blurry, which is why the two are often confused.

In this article, I will explain what each approach is, who owns it, and how they work together. You will learn how to choose the right approach for your organization and how a platform like Roz can support audit workflows. By the end, you'll understand the differences between continuous auditing and continuous monitoring and be better equipped to determine which approach best fits your needs.

What Is Continuous Auditing?

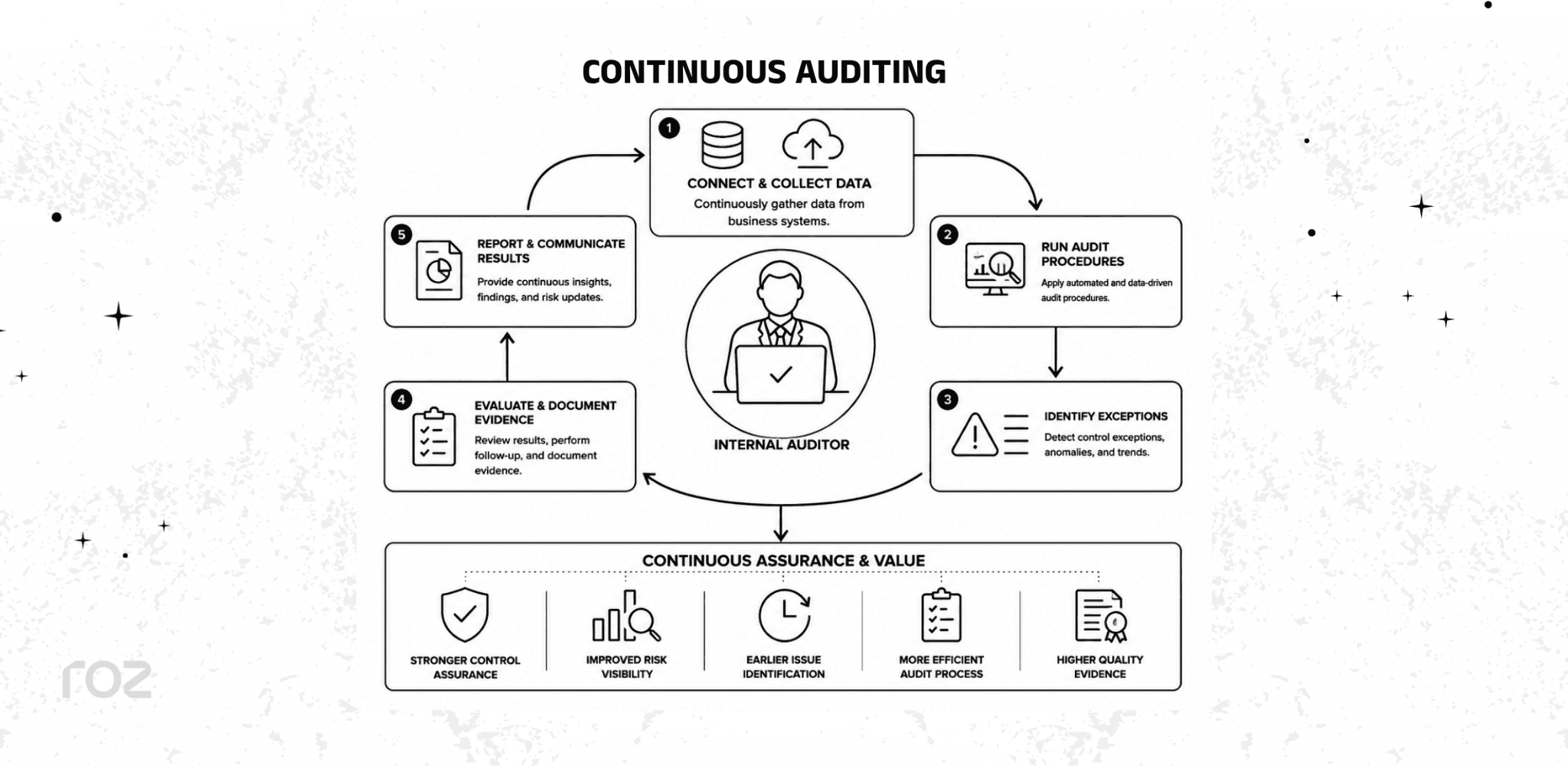

Continuous auditing is an audit methodology that enables auditors to perform audit activities on a more frequent or ongoing basis rather than relying solely on periodic reviews. Continuous auditing is defined by the Institute of Internal Auditors as "any method that allows auditors to perform audit-related activities on a more continuous or continual basis."

Independent assurance is the goal. Continuous auditing relies less on point-in-time testing. With continuous auditing, auditors can examine controls as well as analyze transactions and evidence more frequently. Testing may occur daily, weekly, monthly, or in response to defined business events.

Most of the time, continuous auditing is performed by the internal audit function or independent assurance professionals. Continuous auditors can design the rules, thresholds, and controls for the analytics used to assess the performance of controls throughout the year. They also maintain independence from the processes they audit.

Some of the more common continuous auditing procedures are:

Continuous testing: More frequent evaluation of controls than the single annual evaluation.

Exception-based auditing: Evaluation of transactions that fall outside of established thresholds.

Automated audit analytics: Use of rules to examine entire data sets to identify exceptions.

Continuous evidence review: Routine review of audit evidence (for example, journal entries, access logs, reconciliations, system activity reports, etc.) to support ongoing audit procedures.

Risk-based auditing: Focus of testing on the processes that are the most valuable or carry the most risk.

For example, an internal audit team may utilize analytics to assess journal entries and access controls over the course of the year instead of waiting until the year-end close. This identifies issues sooner and helps them prepare for external reviews.

Continuous auditing allows independent assurance to evaluate controls and offer more frequent reviews to stakeholders utilizing technology and data analytics.

What Is Continuous Monitoring?

Continuous monitoring involves reviewing management activities on an ongoing basis. Some monitoring activities may be conducted in real time, while others may be conducted in a timely manner or on a routine basis.

Management is accountable for continuous monitoring. Overall, internal controls are monitored and operated with support from finance, IT, compliance, and risk management. Process owners also play a key role. These individuals are responsible for the process on a day-to-day basis and are best positioned to respond to alerts in a timely manner.

Monitoring systems track thresholds, exceptions, and anomalies across workflows. Some systems may also be designed to monitor:

Failed approvals: Identifying processes that have not been signed off.

Duplicate payments: Flagging duplicate payments processed for the same transaction.

Unauthorized access: Identifying user access that creates segregation-of-duties conflicts.

Configuration drift: Identifying system settings that have changed without a request.

Late reconciliations: Identifying balance sheet accounts that have not been reconciled in a timely manner.

Compliance alerts: Triggered when a process is completed that violates a defined policy or control rule.

Continuous monitoring is not meant to be an independent assurance activity. While it provides a basis for reinforcing both control and accountability, it does not replace an audit.

Continuous Auditing vs Continuous Monitoring

Although both rely on automation and ongoing data analysis, continuous auditing and continuous monitoring have different objectives, owners, and outcomes. The table below sets them side by side.

Factor | Continuous Auditing | Continuous Monitoring |

Purpose | Provide independent assurance over control effectiveness | Detect and address operational issues quickly |

Owner | Internal audit | Management |

Primary Users | Auditors and audit leadership | Process owners and operations teams |

Frequency | Recurring based on the audit plan (for example, daily, weekly, monthly, or event-driven) | Ongoing based on business needs (real time, near real time, or scheduled) |

Scope | Controls, transactions, and risks within the audit scope | Business processes, operational controls, and compliance activities |

Output | Audit evidence, findings, workpapers | Alerts, dashboards, metrics |

Examples | Reviewing journal entries, access controls | Duplicate payments, failed approvals |

Technology | Audit analytics platforms | ERP systems, SIEM platforms, Continuous Controls Monitoring (CCM) solutions, dashboards, and workflow automation |

Decision Maker | Internal auditor | Process owner or manager |

Goal | Strengthen governance and audit coverage | Support prevention and faster response |

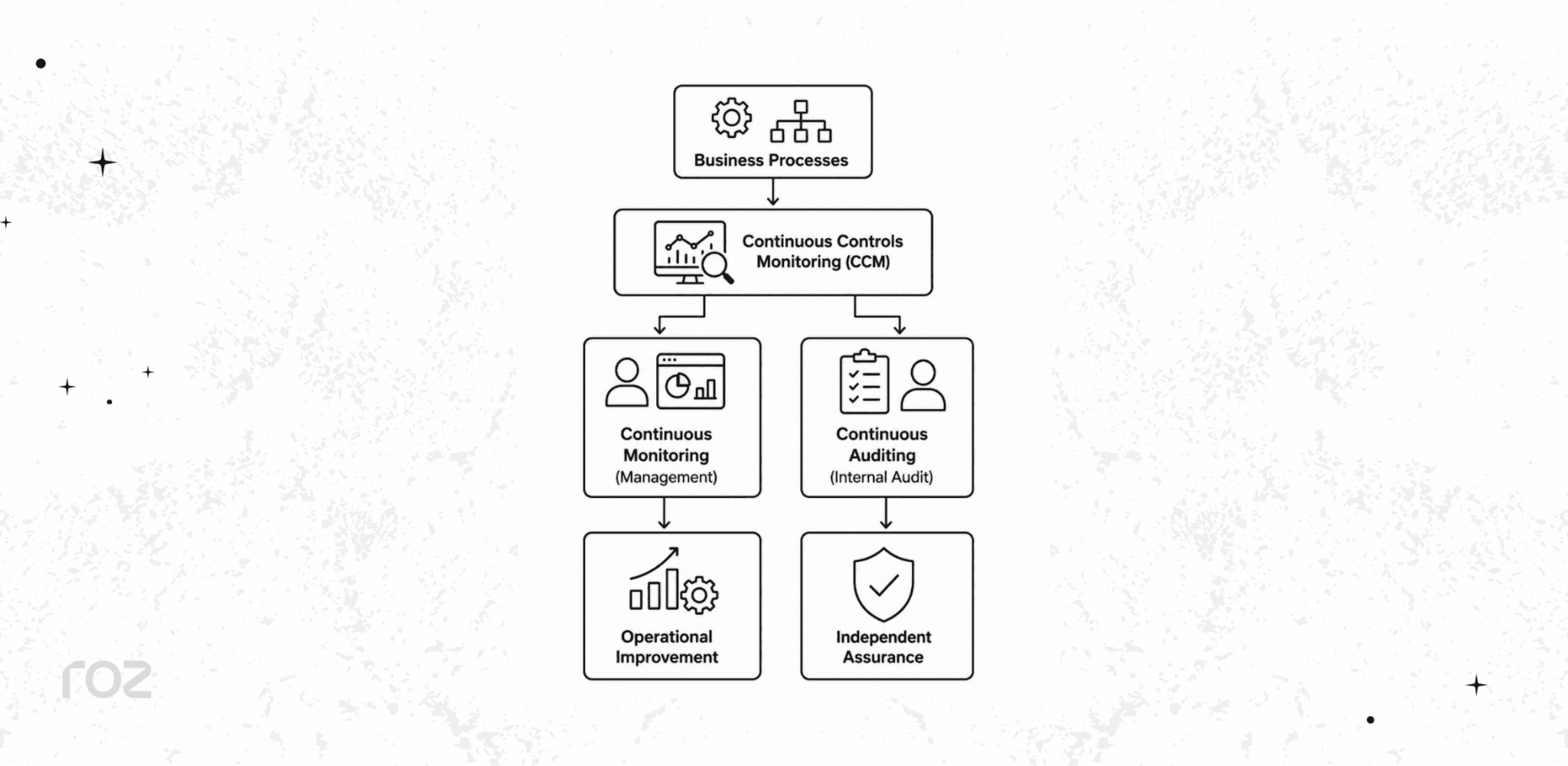

Continuous Controls Monitoring (CCM): Where Does It Fit?

Continuous Controls Monitoring (CCM) continuously checks whether controls are functioning as designed. It is a layer of technology between operational activity and independent assurance. CCM can provide information that is useful to both management and auditors.

Here is how the layers connect:

CCM makes it possible to monitor entire transaction populations or large volumes of transactions using predefined monitoring rules and reduces the need for manual review of routine control activities. CCM supports management via continuous monitoring. In addition, CCM provides information to auditors when they are planning and performing continuous auditing activities.

Trusted CCM systems are directly integrated with your organization's enterprise resource planning (ERP) systems to continuously collect control data. CCM systems generate alerts or trigger workflow notifications when control failures or transactional exceptions occur. This allows management to take the necessary actions and auditors to review the same exception logs to focus their testing on the highest risk control areas.

Benefits of Continuous Monitoring

Continuous monitoring enables management to obtain oversight of day-to-day operations within a much shorter time frame. The main benefits of continuous monitoring include:

Control exceptions and operational issues are identified faster and more easily and can be corrected before they worsen.

Operational resilience is enhanced as disruptions are detected as they occur.

Visibility of compliance is improved throughout processes and tiers.

Time-consuming, tedious manual monitoring effort is reduced through configured rules and notifications.

Exceptions are more easily resolved as they are directed to the appropriate personnel.

Risk management is enhanced due to ongoing visibility of control performance.

Benefits of Continuous Auditing

Strengthening the assurance function of continuous auditing has many benefits, including:

Assurance becomes more timely because auditors can rely on recurring audit procedures rather than periodic testing alone.

Audit coverage is also enhanced, as auditors can analyze, in their entirety, the populations of transactions. Within continuous auditing, sampling will still be permitted.

Better risk optimization and continuous auditing will help us assess and audit the higher-risk areas first.

Repetitive manual testing activities can be reduced, and auditors will be able to devote their attention to the analysis of higher-risk issues.

Timely identification of deficiencies in controls is achieved.

Audit plans will be optimized by reviewing results from monitoring and CCM.

Continuous monitoring results can help inform risk-based audit planning.

Choosing the Right Approach

The right approach depends on your role and what you need to accomplish.

Use continuous monitoring if:

You sit on the management or operations side.

You need ongoing operational visibility into processes and controls.

You need immediate alerts when something goes wrong.

You are responsible for operating and monitoring internal controls.

Use continuous auditing if:

You are part of the internal audit or independent assurance function.

You need independent assurance over controls.

You test the operating effectiveness of controls.

You perform SOX audits, SOC engagements, internal audits, or other risk and compliance assessments.

Most organizations need both. Continuous Monitoring will assist management in recognizing and addressing operational issues, and Continuous Auditing will provide independent assurance regarding the adequacy and functioning of control frameworks. When both are implemented, they simplify the use of common information, reduce repeated work, and improve governance while reducing the unexpected.

How Roz Supports Continuous Auditing Workflows

Continuous monitoring platforms help management oversee day-to-day operations. Audit teams often need additional capabilities to organize evidence, perform readiness assessments, support control testing, and prepare audit documentation.

Roz is an AI platform built specifically for external audit and advisory firms. It helps teams accelerate evidence collection, perform readiness assessments, and execute control testing across sampled or full populations, with human-in-the-loop validation keeping auditor judgment at the center of every engagement.

Within an engagement, Roz can help firms:

Organize evidence in secure, client-specific workspaces

Review uploaded documentation and surface potential evidence gaps

Extract controls to support testing workflows

Generate AI-assisted first-pass workpapers from firm-approved templates

Maintain source-linked traceability across engagement documentation

Roz supports audit workflows by helping firms streamline documentation and first-pass analysis while keeping auditor review, professional judgment, and final conclusions at the center of the engagement.

Conclusion

Effective governance relies on both continuous monitoring and continuous auditing. Here, continuous monitoring aids management in viewing and reacting to issues, and continuous auditing offers independent assurance.

As audit functions adopt AI, platforms like Roz can help accelerate evidence collection, support readiness assessments, and generate AI-assisted first-pass workpapers. This allows auditors to spend more time evaluating evidence, exercising professional judgment, and delivering high-quality audit outcomes.

Organizations should first determine which controls require ongoing operational monitoring and which require independent audit evaluation. This distinction helps organizations strengthen governance, improve control oversight, and support more effective audit planning.

Frequently Asked Questions

Is continuous monitoring part of continuous auditing?

No, they are separate. Management owns continuous monitoring for operational oversight, while internal audit owns continuous auditing for independent assurance.

Who is responsible for continuous monitoring?

Management owns continuous monitoring, supported by finance, IT, and compliance teams who own the underlying controls and processes.

What is Continuous Controls Monitoring (CCM)?

CCM is a technology-based method for continuously evaluating controls. It allows teams to monitor all transactions instead of just a sample.

Does continuous auditing replace internal audits?

No, it is a method used by internal auditors to improve efficiency. Auditors still plan engagements, evaluate evidence, and form conclusions.

Can AI be used in continuous auditing?

Yes. AI can help with tasks like organizing evidence and detecting anomalies, but auditors remain responsible for forming conclusions.

Is continuous auditing required for SOX?

No, but it is a highly effective method for supporting SOX compliance by enabling more frequent and comprehensive control testing.