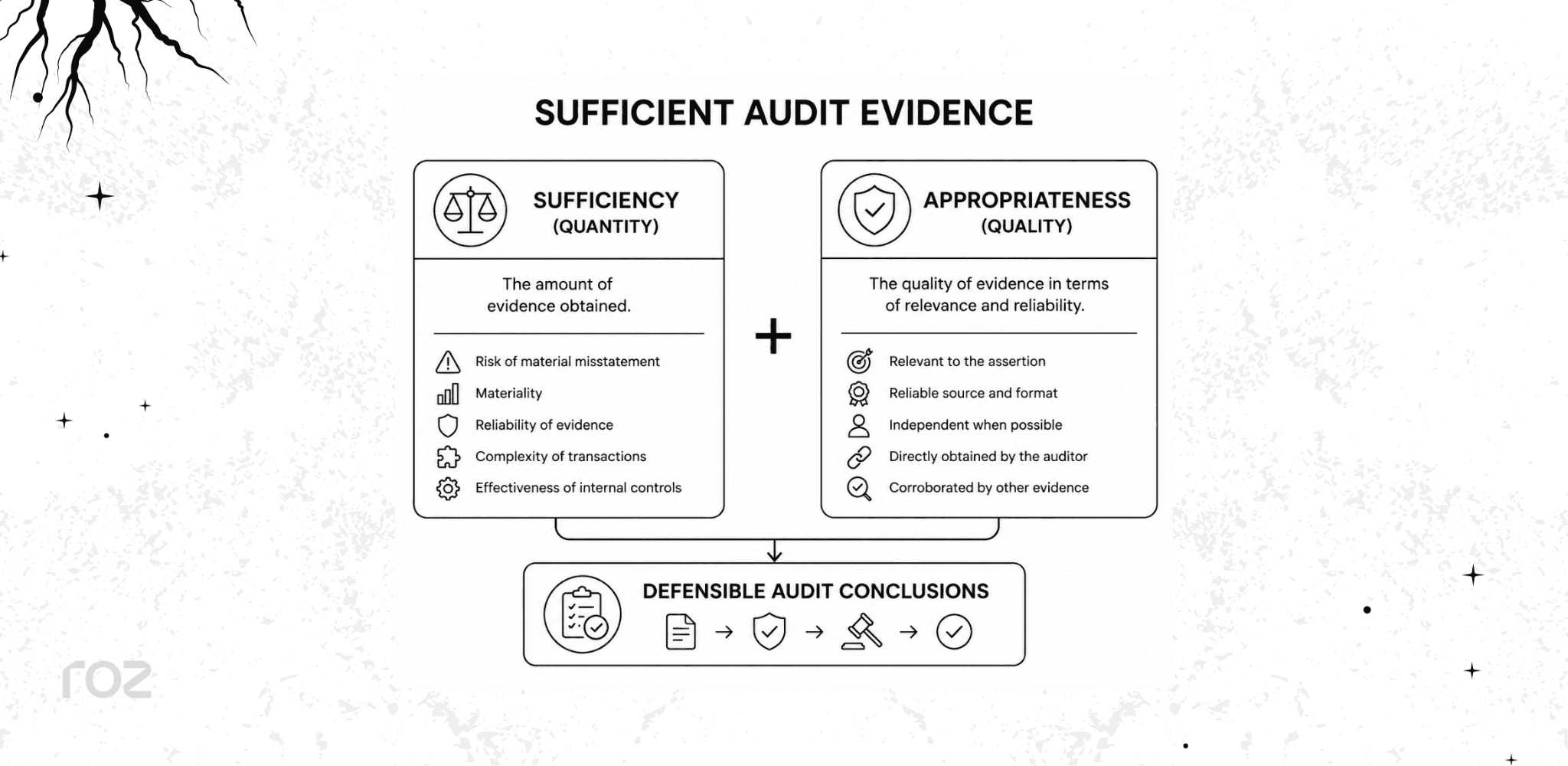

Sufficient Audit Evidence: A Practical Guide for Auditors

Most audits do not fail because auditors lack evidence. They fail because they lack sufficient, reliable, and traceable evidence to support their conclusions. Knowing when you have gathered "enough" is one of the hardest judgment calls in any engagement, and it carries real consequences when a regulator, peer reviewer, or inspector revisits your file.

That challenge is getting harder, not easier. Engagement teams now work with more data, more file formats, and more client-provided reports than ever before. Evidence overload has become its own problem: piles of documents do not equal a defensible conclusion. At the same time, AI tools, modern compliance programs, and digital workflows are changing how teams collect, organize, and trace evidence.

In this article, I will walk you through what you need to know. You will learn how to tell whether your evidence is sufficient; which evidence carries the most weight; the common mistakes that leave files exposed; and a practical framework you can apply on your next engagement.

What Is Sufficient Audit Evidence?

Sufficient audit evidence is the quantity of relevant and reliable information that an auditor obtains to reduce audit risk to an acceptably low level and to support the conclusions on which the audit opinion is based.

Two ideas sit at the center of this:

Sufficiency is about quantity - how much evidence you gather.

Appropriateness is about quality - how relevant and reliable that evidence is.

A simple way to think about it is:

Effective Audit evidence = Sufficiency + Appropriateness

These two factors work together. Higher-quality evidence may reduce the amount of evidence required. However, gathering more low-quality evidence does not compensate for poor reliability. PCAOB AS 1105 says, "Getting more of the same type of audit evidence... can't make up for the bad quality of that evidence." In practice, auditors aim to collect enough high-quality evidence to support defensible conclusions—not the largest possible volume of documentation.

Why Does Sufficient Audit Evidence Matter for Audit Quality?

Sufficient evidence is what stands behind your conclusions when someone asks you to defend it. Without it, the conclusion rests on assertion rather than proof.

Strong evidence delivers several outcomes:

It supports defensible audit conclusions.

It reduces audit risk to an acceptable level.

It strengthens overall audit quality.

It improves confidence among stakeholders who rely on the financial statements.

It helps the file withstand peer reviews and regulatory inspections.

The downstream effect of weak evidence is direct. A poorly supported audit file gets flagged in an inspection, a conclusion gets challenged, and the firm absorbs rework, increased scrutiny, and reputational risk.

What Is the Difference Between Sufficient and Appropriate Audit Evidence?

Sufficiency and appropriateness are related but distinct. The table below breaks down each component and what it looks like in practice.

Component | Meaning | Example |

Sufficiency | Amount of evidence | Testing 100 invoices |

Appropriateness | Quality of evidence | A bank confirmation |

Relevance | Related to the assertion | An inventory count for existence |

Reliability | Trustworthiness of the source | Third-party records |

Think of quality as weight. High-quality evidence may reduce the amount of evidence required to reach a solid conclusion.

What Standards Govern Audit Evidence Globally?

Audit evidence requirements are governed by two primary sets of standards, with the applicable set determined by the location and nature of the audit.

International (ISA):

ISA 500 (Audit Evidence) sets the auditor's responsibility to design and perform procedures that obtain sufficient appropriate audit evidence to support audit conclusions.

ISA 315 focuses on identifying and assessing the risks of material misstatement, including understanding the entity and its controls.

ISA 330 requires the auditor to respond to those assessed risks, calling for more persuasive evidence as risk rises.

United States (PCAOB):

PCAOB AS 1105 (Audit Evidence) explains what counts as audit evidence and how to obtain sufficient appropriate evidence.

PCAOB AS 2301 (The Auditor's Responses to the Risks of Material Misstatement) sets requirements for designing responses to assessed risks.

The pattern across both frameworks is the same: assess the risk first, then gather evidence proportionate to that risk.

How Do Auditors Determine Whether Evidence Is Sufficient?

There is no universal formula. Sufficiency comes down to professional judgment, guided by five factors.

Risk Assessment

The higher the risk of material misstatement, the more persuasive and extensive the audit evidence generally needs to be. AS 1105 puts it plainly: as risk increases, the amount of evidence the auditor should obtain also increases. High-risk areas that typically demand more evidence include:

Revenue recognition

Related-party transactions

Manual journal entries, especially those posted at period-end

Materiality

Materiality shapes the scope and focus of your testing. More material areas often require more extensive testing, particularly when combined with higher risk. Areas that often warrant additional attention include:

High-value accounts

Significant disclosures

Reliability of Evidence

More reliable evidence reduces the volume you need. Evidence from an independent external source, obtained directly by you, in documentary or system-generated form, carries the most weight. Weaker evidence calls for corroboration from additional sources.

Complexity of Transactions

Complex transactions involve more judgment, which raises the bar for evidence. Examples include:

Fair value estimates

Cloud-based IT environments

AI governance processes

Effectiveness of Internal Controls

When a client's controls operate effectively, auditors may be able to rely on them and reduce substantive testing. When controls are weak or untested, you need more direct, substantive evidence to fill the gap.

What Is the Audit Evidence Reliability Hierarchy?

Not all audit evidence has the same value. Auditors rank evidence based on its reliability, though the specific context of the audit is always the most important factor. The following list arranges evidence types from most to least reliable.

External confirmations

Physical inspections

Auditor reperformance and recalculations

Direct observations

Internal records supported by effective controls

Management inquiries and oral explanations

Three principles explain the ranking:

External beats internal: Independent sources are more reliable than company-generated records.

Documentary beats oral: A written record carries more weight than a verbal explanation.

Directly obtained beats indirectly: Evidence obtained directly by the auditor is more reliable than evidence handed to you.

One caution worth repeating: inquiry of company personnel, on its own, does not provide sufficient evidence to support a conclusion.

Common Types of Audit Evidence (With Examples)

Audit procedures produce different types of evidence. The table below pairs each procedure with a practical example.

Procedure | Example |

Inspection | Reviewing contracts and supporting documents |

Observation | Observing physical inventory counts |

Confirmation | Obtaining bank confirmations |

Recalculation | Verifying depreciation calculations |

Reperformance | Reperforming a user access review |

Analytical procedures | Performing trend analysis |

Inquiry | Interviewing process owners |

Audit Evidence vs. Audit Documentation: What Is the Difference?

These two terms are often used interchangeably, but they are not the same.

Audit evidence is the information auditors use to support their conclusions.

Audit documentation is the record that demonstrates the work you performed.

Here is how each looks in practice:

Audit evidence | Audit documentation |

Invoices | Workpapers |

System logs | Testing summaries |

Bank confirmations | Reviewer sign-offs |

Evidence answers the question "What supports my conclusion?" Documentation answers "Can the work performed be demonstrated and traced?"

How to Evaluate Audit Evidence Sufficiency: A 5-Step Framework

Use this model to test whether your evidence holds up before you sign off.

Verify relevance. Ask: Does this evidence support the assertion you are testing?

Validate reliability. Ask: Can the evidence be trusted, given its source and format?

Check completeness. Ask: Is the population you tested complete?

Corroborate information. Ask: Can another independent source confirm this?

Assess traceability. Ask: Can your conclusion be linked back to the source evidence?

These steps work together. If one area reveals a weakness, auditors may need to perform additional procedures before concluding that the evidence is sufficient.

What Are the Common Signs of Insufficient Audit Evidence?

Certain patterns signal that a file may not hold up. Watch for:

Overreliance on management explanations

Missing supporting documentation

Conflicting information across sources

Unvalidated client-produced reports

Sample sizes too small for the risk

Incomplete or broken audit trails

Incomplete populations

Any one of these is a prompt to perform additional procedures before concluding.

How Does Roz Help Firms Improve Evidence Sufficiency Workflows?

Checking whether evidence is complete, relevant, and sufficient often takes significant manual effort. Roz is an AI platform built specifically for external audit and advisory firms. It helps teams accelerate evidence collection, perform readiness assessments, and execute control testing, while keeping auditor judgment at the center of every engagement.

For evidence sufficiency workflows, Roz can help:

Centralize evidence in client-specific workspaces

Surface potential evidence gaps earlier in the engagement

Improve traceability with source-linked documentation

Generate AI-assisted first-pass workpapers from firm-approved templates

Support reviewers with organized, evidence-backed outputs

Roz helps streamline audit workflows and reduces administrative effort. Auditor review, professional judgment, and final conclusions remain essential to the engagement.

Conclusion

Sufficient audit evidence isn't about collecting more documents but collecting the right ones. Your evidence must be relevant, reliable, complete, corroborated, and traceable. As audits become more digital, the focus is expanding beyond sampling to include evidence traceability and source validation. Can you trace every conclusion back to its source?

Firms that build repeatable evidence workflows now will be better positioned for the future. Explore how Roz helps audit teams streamline evidence collection, improve traceability, and reduce manual administrative effort.

Frequently Asked Questions

What's the difference between sufficient and appropriate audit evidence?

Sufficiency is the quantity of evidence; appropriateness is its quality (relevance and reliability). You need both. More high-quality evidence means you need less of it, but no amount of low-quality evidence can compensate for its poor quality.

How do auditors determine if evidence is sufficient?

Auditors use professional judgment, considering five key factors: risk of material misstatement, materiality, evidence reliability, transaction complexity, and the client's internal controls.

What makes audit evidence reliable?

Reliability depends on its source and format. Evidence is more reliable if it comes from an independent external source, is in its original documentary form, and is obtained directly by the auditor.

What is the difference between audit evidence and audit documentation?

Audit evidence is the information used to form a conclusion (e.g., invoices, bank confirmations). Audit documentation is the record of the work performed (e.g., workpapers, sign-offs). Evidence supports the opinion; documentation proves the work was done.