Why Audit Firms Are Moving Beyond Sampling in 2026

Audit firms are evolving with the modern age by no longer relying on traditional sampling methods. With modern cloud infrastructure, traditional subset testing methods are becoming less effective for highly digital environments. Audit methodologies that were built with paper ledgers in mind are increasingly difficult to apply to modern cloud-native enterprises. As the volume of digital evidence continues to grow, relying on small sample sizes may not fully address the breadth of modern audit risks.

The issue at hand is that the data environments of today are growing rapidly while the accounting workforce in the US has seen drastic declines. Firms must find ways to analyze larger volumes of data with less manual effort. The use of full-population testing is becoming more common as AI and data analytics allow firms to work with entire datasets instead of sample size subsets.

In this article, I will compare and contrast traditional audit sampling methods with modern AI-assisted auditing and continuous auditing methods. I will show the potential of these new methods and explore the operational drivers behind these evolving audit approaches.

What Is Audit Sampling?

Before examining alternative approaches, it is important to understand the fundamentals of audit sampling. Audit sampling is defined as the application of audit testing procedures to a less than 100% selection of the items that comprise an account balance or a class of transactions. The purpose of audit sampling is to assess the attributes of a population, which enables auditors to draw a conclusion about the entire population.

Before the age of digital media, auditors relied on sampling techniques simply because if they were manually tracing cash movements via paper invoices, reviewing several million transactions was operationally impractical.

Statistical vs. Judgmental Sampling

There are two primary techniques auditors employ when they are selecting samples: statistical and judgmental.

Statistical sampling requires an auditor to select a sample based on the principles of probability and subsequently evaluate the findings of that sample. Because every item in the population has the same probability of being analyzed, auditors can quantify the level of risk attributable to the sample and then state their level of confidence in the findings.

Judgmental (or non-statistical) sampling is the practice of selecting items for review that the auditor believes will present the greatest risk, using the judgment of the auditor. This practice does not enable the auditor to quantify the risk levels associated with the sample but does allow them to focus on an area of concern.

Determining Sample Size

Deciding how many items you want to test is critical, and this is a sample size calculation that is influenced by a number of the variables of interest, such as overall population size. This is a balance between auditing and ascertaining, via sampling, operational efficiency and error rate. For traditional audits, this meant performing complicated calculations just to come up with a standardized sample size that would provide sufficient audit assurance in balance with optimal audit efficiency.

How Traditional Sampling Works

When performing traditional sampling, auditors use a periodic testing method to assess the effectiveness of organizational controls. During this method, auditors select a sample of inputs from a population of transactions, request evidence and supporting documentation from management, and review the evidence to assess the effectiveness of controls during the period of the test. In many cases, the workflows of this method depend on:

Spreadsheets

Email evidence requests

Manual walkthroughs

Shared file storage systems

Workpaper documentation processes

The method of traditional sampling has been in use for a long time; however, it may be operationally expensive in cases where there are a lot of transactions, especially if they are dispersed in many locations.

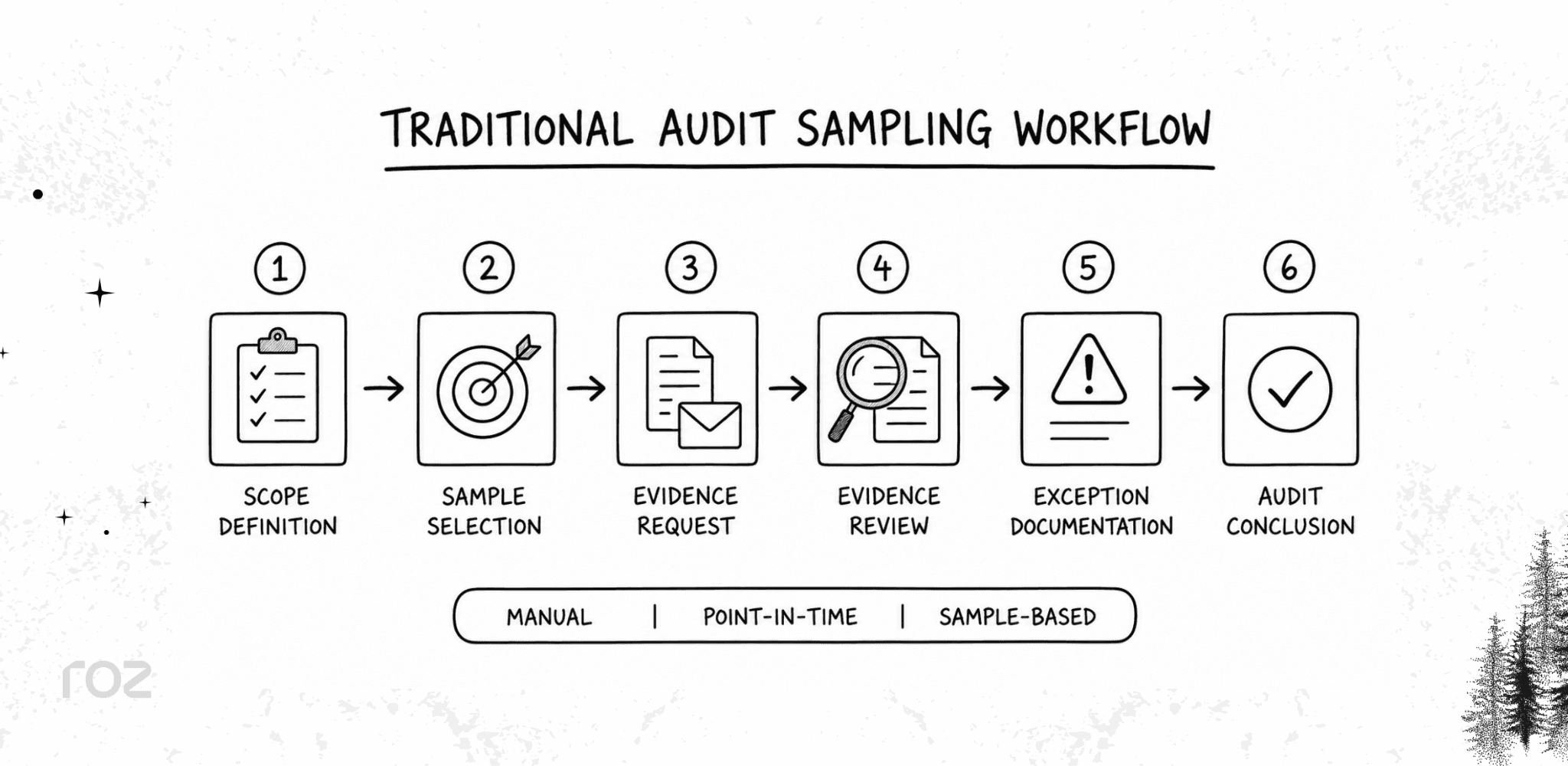

Example of a Traditional Audit Sampling Workflow

A manual audit review of evidence will often follow the same general steps:

Scope Definition: Selecting the control, process, or transaction population to be tested during the audit.

Sample Selection: Identify a sample using a statistical or judgmental approach to select the sample population.

Request Evidence: Submit a request to management to provide the transaction sample and supporting documentation such as approvals, access logs, reports, records of changes, policy acknowledgments, or evidence.

Evidence Review: Perform a manual review of evidence to determine whether controls were implemented and operating as intended.

Document Exceptions: Record any of the issues identified during the review, including the absence of approvals, insufficient or lack of evidence, deviation from controls, or timing issues.

Audit Opinion: Describe the outcomes of the review and determine whether the control under review was appropriately designed and operating effectively for the audit objective.

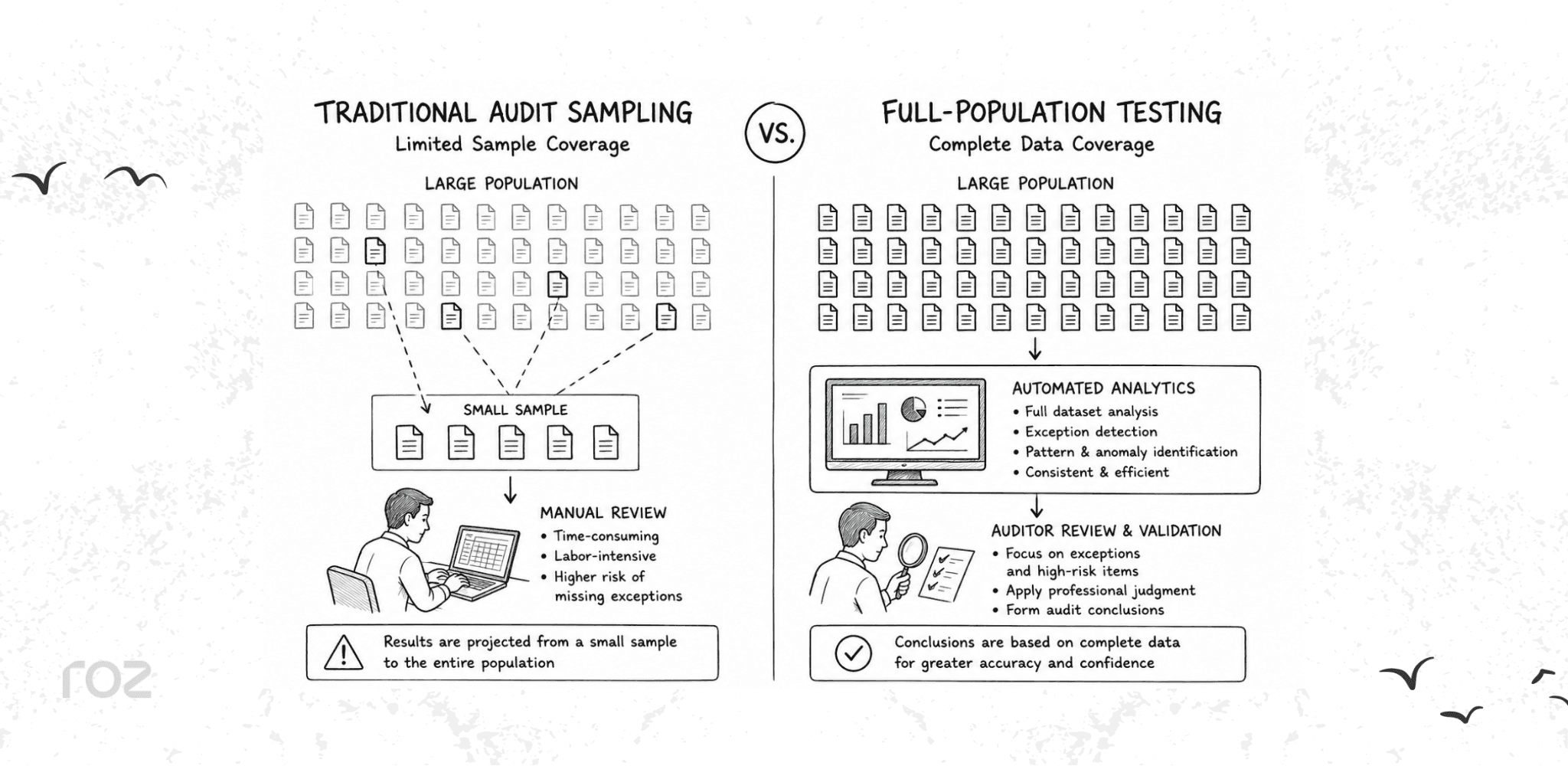

The Limitations of Sampling in Modern Audits

Audit sampling is still valid in many scenarios, but older sampling methods are increasingly difficult to apply within modern business environments. Rapidly scaling businesses have increased technological complexity. The limitations of sample-based testing are now more apparent.

Increasing Complexity of Enterprise Systems: Modern businesses operate in multiple regions and environments that are integrated with many SaaS applications, the cloud, and large ERP systems. This leads to audit evidence being dispersed across many platforms, making it hard to collect a complete population for sufficient manual testing.

Fraud and Risk Detection Challenges: The main issue of sampling is that testing a limited sample population may not identify rare or isolated exceptions. A sample of 40 transactions from a population of 40,000 leaves much of the population untested, which can easily lead to unauthorized access, configuration drift, and other rare, hard-to-identify exceptions.

Growing Regulation and Client Demands: Clients now expect shorter audit times with higher-quality evidence and continuous monitoring of controls. The old way of manually sampling creates bottlenecks and is unable to meet the new standard of automated and continuous auditing.

What Is Full-Population Testing?

Full-population testing is the opposite of the traditional method of sampling. Automation and audit analytics allow for a full assessment of a population. Assessing an entire population can be resource-intensive, but it may provide broader visibility into structured digital environments.

Full-Population Testing vs Audit Sampling

This distinction is important. Traditional sampling may remain appropriate when evidence is physical, judgmental, or difficult to standardize. Full-population testing is generally more effective when evidence is digital, structured, and available at scale.

Feature | Traditional Sampling | Full-Population Testing |

Scope | Small transaction subsets | Entire transaction populations |

Timing | Periodic, point-in-time reviews | Continuous or high-frequency analysis |

Method | Manual testing and review | Automated analytics and AI testing |

Visibility | Limited anomaly detection | Broader risk detection and coverage |

Benefits of Full-Population Testing

Implementing full population testing provides immediate benefits. It provides better outlier detection by spotting all outliers in the population. It shortens the testing cycles, completed more quickly by automated scripts than manual reviewers. Additionally, it enables continuous control monitoring, identifying control failures as they occur rather than months later.

The Role of AI in Modern Audits

There is a growing integration of AI into contemporary audit and compliance workflows. The ability to use AI during the testing phase of audits does not replace the auditor's judgment. AI helps scale the review of evidence and empowers audit teams to analyze larger and more complex datasets more efficiently.

AI-Assisted Evidence Review

AI can classify evidence, identify policy and data discrepancies, and flag exceptions. Automating portions of these reviews allows auditors to focus more on exception analysis and professional judgment. AI may, for instance, help in reviewing user access certifications for audits and assist in the detection of missing documentation.

Continuous Auditing and Automated Monitoring

There is more AI- and automation-led continuous auditing today. Organizations can continuously collect evidence, monitor controls in real time, and generate automated alerts. Organizations move from periodic control assessments to audits of controls integrated into operations, which is a significant improvement for organizations operating in a cloud environment.

Why AI Does Not Replace Auditors

Although AI can perform analysis and handle the first review, human oversight remains essential. Professional judgment and contextual interpretation remain core auditor responsibilities. AI can assist auditors in identifying whether controls remain effective and whether exceptions require additional review.

How Roz Helps Audit Firms Move Beyond Sampling

Roz is an AI-native engagement and audit-delivery platform designed for CPA firms and advisory teams performing control-based reporting engagements. Roz, acting as an intelligent enterprise data room, supports firms in evolving their evidence-based audit workflow while still allowing auditors to retain control.

AI-Assisted Evidence Testing: Roz evaluates policies, procedures, and evidence to identify documentation gaps before testing begins. This feature significantly reduces the amount of manual verification that users need to do.

Secured Audit Workspaces: Roz has secure, client-specific workspaces that consolidate evidence and audit trails. It helps keep documentation organized and aids accessibility.

AI-Assisted Control Mapping: Roz retrieves controls from policies, enabling teams to measure documentation against frameworks and requirements efficiently, with a minimal need for spreadsheets.

Enhanced Audit Readiness: By reducing the amount of manual work, Roz helps teams better manage audit readiness workflows, thus improving the visibility of documentation across multiple client engagements.

Conclusion

There are still many cases where practitioners need to rely on traditional audit sampling techniques, but the current audit climate requires wider coverage, quicker evidence, and more flexible testing. Continuous auditing and analytics are helping organizations strike a balance between greater audit coverage, quicker evidence assessment, and support for continuous auditing, all without compromising practitioner oversight and professional judgment.

FAQs

What is full-population testing in auditing?

Full-population testing is a modern audit technique that leverages data analytical tools and automation to assess all transactions or records (100%) within a population, as opposed to relying on a sample. This technique enhances the ability to identify outliers and provides broader visibility into digital transaction populations.

What are the benefits of continuous auditing?

The ability to conduct real-time control testing and risk assessment is the foundational benefit of continuous auditing. Improvements in the identification of control breakdowns, a decrease in year-end audit stress and support for a more proactive approach to risk management are the benefits of continuous auditing.

Can small audit firms use AI audit platforms?

Yes. Numerous new AI audit platforms (e.g., Roz) provide audit firms with scalable infrastructure and usage-based pricing. For small and mid-size audit firms, this solution offers scalable automation workflows for handling a volume of audits without proportional increases in staff.